Design and Estimation of a Taxpayer Compliance Model from a Behavioral Economics Perspective Considering Economic and Situational Factors

Keywords:

Tax compliance, behavioral economics, meta-synthesis, tax attitude, institutional trust, social norms, Shannon entropy, tax policy-makingAbstract

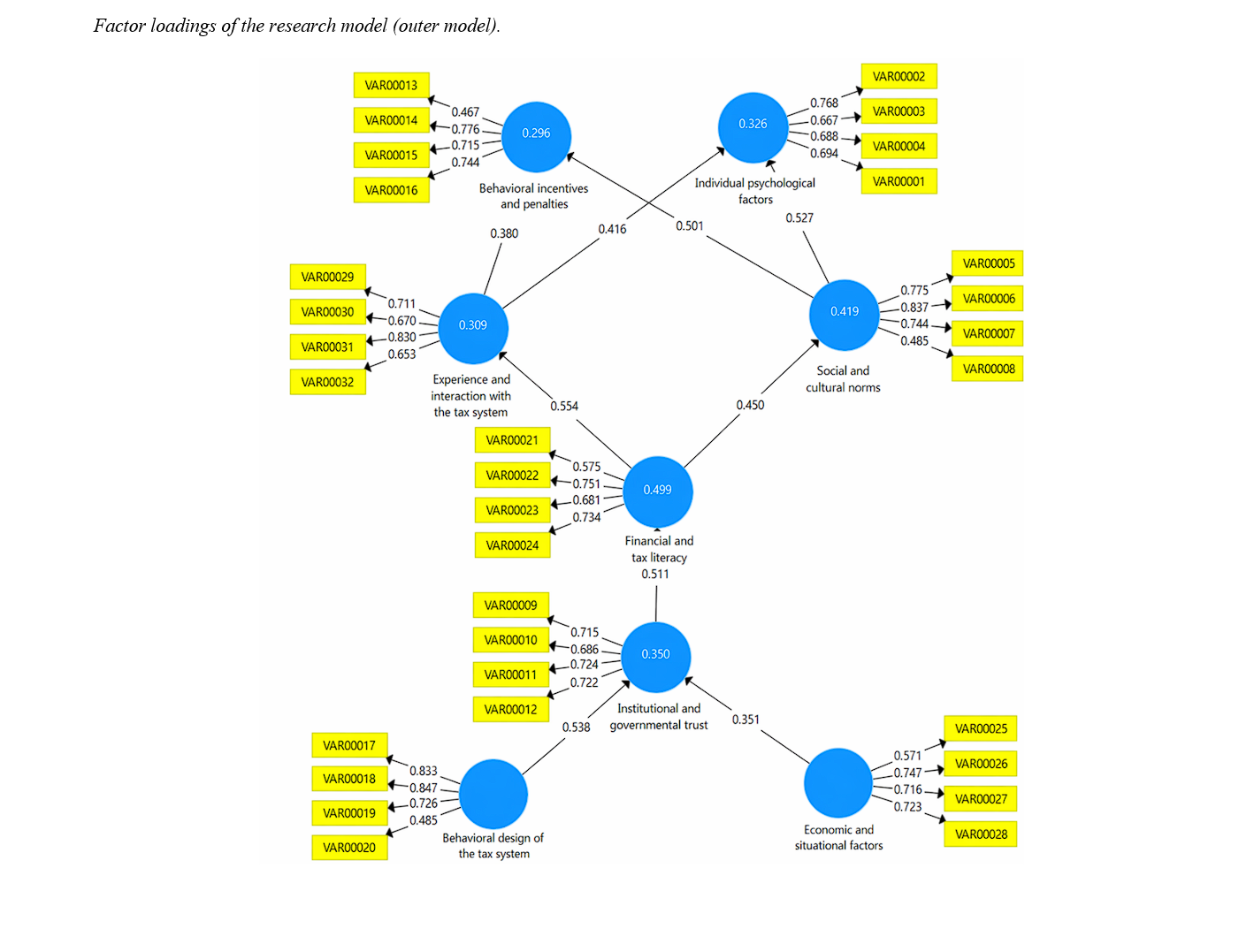

This study was conducted with the aim of designing and estimating a model of taxpayer compliance from the perspective of behavioral economics, taking into account economic and situational factors. In terms of purpose, the present study is applied, and in terms of nature, it is descriptive–analytical and of a survey type. In the first stage, in order to identify and level the factors affecting taxpayer compliance, the Interpretive Structural Modeling (ISM) method was employed using the opinions of experts in the field of taxation. At this stage, eight main components—including individual psychological factors, social and cultural norms, institutional and governmental trust, behavioral incentives and penalties, behavioral design of the tax system, financial and tax literacy, economic and situational factors, and experience and interaction with the tax system—were identified, and their internal relationships were analyzed through the Structural Self-Interaction Matrix (SSIM), the reachability matrix, and the final reachability matrix. The leveling results indicated that some variables play a driving and foundational role, while others are more influenced by other factors. The MICMAC (cross-impact matrix multiplication applied to classification) analysis also confirmed that infrastructural components such as the behavioral design of the tax system and economic and situational factors fall into the category of independent and driving variables and possess the highest level of influence within the system, whereas variables such as individual psychological factors and experience of interaction with the tax system are primarily categorized as dependent variables. In the second stage, in order to fit and validate the extracted model, Structural Equation Modeling (SEM) with a Partial Least Squares (PLS-SEM) approach was applied. The data for this section were collected through a questionnaire with the participation of 317 experts from the National Tax Administration. The results of the multicollinearity test indicated that the Variance Inflation Factor (VIF) values for all constructs were below the threshold level, suggesting no multicollinearity issue. Additionally, reliability indices including Cronbach’s alpha and composite reliability for all variables were above 0.7, and the Average Variance Extracted (AVE) was above 0.5, indicating acceptable reliability and convergent validity of the measurement instrument. Discriminant validity was also confirmed using the Fornell–Larcker criterion and the Heterotrait–Monotrait ratio (HTMT). The coefficient of determination (R²) for endogenous constructs was evaluated at an acceptable level, and the effect size and predictive power indices indicated good model fit and satisfactory predictive capability. Overall, the findings of the study indicate that taxpayer compliance is a multidimensional phenomenon that, in addition to economic variables, is significantly influenced by behavioral, institutional, and system design mechanisms. Improving taxpayer compliance therefore requires the adoption of an integrated approach grounded in behavioral economics, along with the strengthening of institutional and technological infrastructures.

References

Antinyan, A., & Asatryan, Z. (2024). Nudging for tax compliance: A meta-analysis. The Economic Journal. https://doi.org/10.1093/ej/ueae088

Barghi Osgouei, M. M., Namazi, F., & Pourmahdi, H. (2024). Factors Affecting Taxpayers' Tendency Toward Tax Evasion https://civilica.com/doc/2221377

Bavaghar, M., & Sarchami, M. (2025). Examining the Effect of Establishing the Taxpayer System and Point-of-Sale Terminals on Tax Culture Sari. https://civilica.com/doc/2531314

Burgstaller, L., & Pfeil, K. (2024). You don’t need an invoice, do you? An online experiment on collaborative tax evasion. Journal of Economic Psychology, 101, 102708. https://doi.org/10.1016/j.joep.2024.102708

Damiri, A., Shahrestani, S., & Zahmatkesh, Z. (2025). Examining the Effect of Selected Tax Factors and Social Norms on Tax Compliance Sari.

Dimitras, A., Fourlas, V., Kirchler, E., & Peppas, G. (2025). Drivers of tax compliance: Survey evidence from 1761 Greek micro-firms. Journal of Behavioral and Experimental Economics, 119, 102480. https://doi.org/10.1016/j.socec.2025.102480

Esmaeilvand, I. (2025). The Role of the Taxpayer System in the Digital Transformation of Iran's Value-Added Tax System: Challenges, Consequences, and Implementation Requirements Astara. https://civilica.com/doc/2462227

Falsetta, D., Schafer, J. K., & Tsakumis, G. T. (2024). How government spending impacts tax compliance. Journal of Business Ethics, 190(2), 513-530. https://doi.org/10.1007/s10551-023-05383-3

Farrar, J., & King, T. (2023). To punish or not to punish? The impact of tax fraud punishment on observers’ tax compliance. Journal of Business Ethics, 183(1), 289-311. https://doi.org/10.1007/s10551-022-05061-w

Frecknall-Hughes, J., Gangl, K., Hofmann, E., Hartl, B., & Kirchler, E. (2023). The influence of tax authorities on the employment of tax practitioners: Empirical evidence from a survey and interview study. Journal of Economic Psychology, 97, 102629.

Jabbari Khouzani, A. (2024). The Effect of the Ratio of Assessed Tax to Declared Tax on Tax Compliance with Emphasis on the Role of the Comprehensive Tax Plan in Large Companies of Khuzestan Province Aliabad. https://civilica.com/doc/2284849

Lohse, J., Rahal, R. M., Schulte-Mecklenbeck, M., Sofianos, A., & Wollbrant, C. (2024). Investigations of decision processes at the intersection of psychology and economics. Journal of Economic Psychology, 103, 102741. https://doi.org/10.1016/j.joep.2024.102741

Maleki, E., & Hamdanchi Azad, S. (2025). A Review of the Effects of the Taxpayer System on Accountants' Job Stress: A Promotional Approach Focusing on Psychological, Technological, and Organizational Dimensions Hamedan. https://civilica.com/doc/2380440

Muller, M., Olsen, J., Kirchler, E., & Kogler, C. (2023). How explicit expected value information affects tax compliance decisions and information acquisition. Journal of Economic Psychology, 99, 102679.

Murakami, Y., & Taguchi, S. (2025). How gender and prosociality affect machine interaction in tax compliance: A game-theoretic experiment. Journal of Behavioral and Experimental Economics, 116, 102369. https://doi.org/10.1016/j.socec.2025.102369

Nathan, B., Perez-Truglia, R., & Zentner, A. (2026). Paying your fair share: Perceived fairness and tax compliance. Journal of Accounting and Economics, 81(2), 101838. https://doi.org/10.1016/j.jacceco.2026.101838

Pourhassan, F., Zadeh, A. H., & Sanavi Gorousian, V. (2024). Examining the Effect of Implementing the Law on Sales Terminals and the Taxpayer System on Taxpayer Satisfaction with the Mediating Role of Non-Presence Services of Tax Systems: A Case Study of Taxpayers of the General Tax Administration of Razavi Khorasan Province Torbat Heydariyeh. https://civilica.com/doc/2211747

Rezvani, N., & Roshanbin, H. (2024). The Effect of Electronic Tax Systems on Increasing Taxpayer Compliance: A Case Study. Journal of Digital Tax Transformation, 2(1), 18-38.

Salmani, H. (2025). Taxpayers' Rights in the Tax Litigation Process Hamedan. https://civilica.com/doc/2340394

Downloads

Published

Submitted

Revised

Accepted

Issue

Section

License

Copyright (c) 2026 Erfan Zolnorian (Author); Gholamreza Farsad Amanollahi; Farrokh Bostani, Ali Nemati (Author)

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.